Who are the HSBC Premier credit card airline and hotel transfer partners?

Links on Head for Points may support the site by paying a commission. See here for all partner links.

18 months ago, HSBC Premier undertook a substantial upgrading of its credit card transfer partners.

What was a bit of a laughing stock – although Avios was also partner – suddenly became a real contender, at least for the airline partners.

Even better, transfers to airline and hotel partners are instant and there is no minimum points transfer.

The only snag is that the HSBC Premier credit card is a faff to get. You need to sign up for free to HSBC’s Premier current account (£75,000 income and a HSBC investment product required) in order to apply for the free Premier credit card and the paid-for Premier World Elite credit card.

The two HSBC credit cards earn as follows:

The free HSBC Premier card, reviewed here, earns 1 HSBC point per £1 spent, which translates to 0.5 airline miles or hotel points.

The representative APR is 23.9% variable.

The £195 HSBC Premier World Elite card, reviewed here, earns 2 HSBC points per £1 spent, which translates to 1 airline mile or hotel point. There is a sign-up bonus of 80,000 points, worth 40,000 airline miles or hotel points, albeit this is spread over two years.

The representative APR is 59.3% variable, including the annual fee. The representative APR on purchases is 18.9% variable.

How to transfer points to travel partners

Annoyingly, it is not possible to make points transfers via the HSBC app. You need to log in to the HSBC UK website using your HSBC Premier details.

One bit of positive news is there are no transfer minimums.

2 HSBC points will get you 1 airline mile or 1 hotel point.

Transfers to some partners are instantaneous

Yes, instant. In the UK points market, this is still rare.

You aren’t at risk of missing out on a redemption by waiting for your HSBC points to go across.

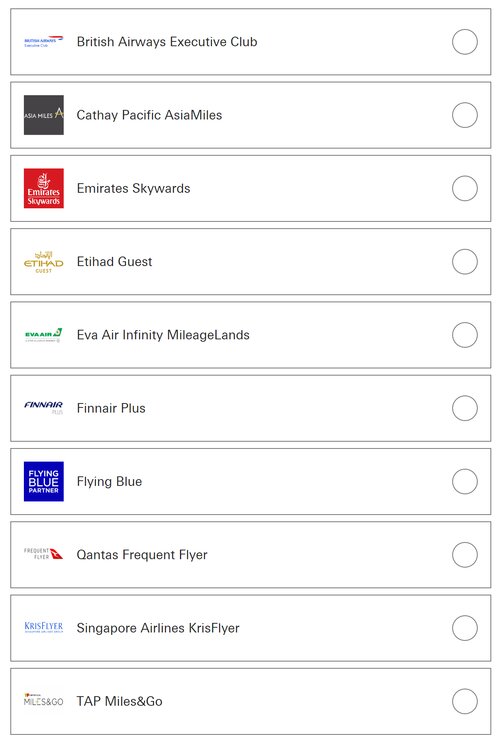

Who are the HSBC Premier credit card travel partners?

Here are the HSBC airline transfer partners:

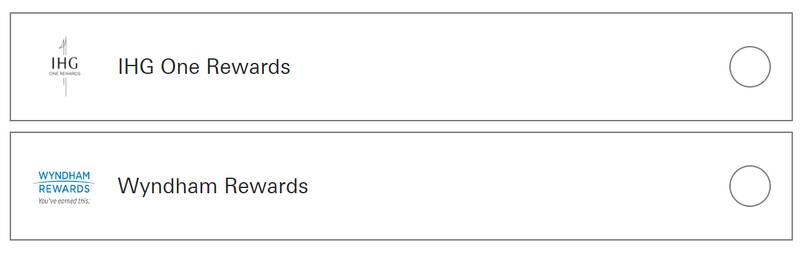

Here are the hotel partners:

Are these transfers good value?

There are two ways of looking at this:

- Are airline and hotel scheme transfers good value compared to redeeming for shopping gift cards etc?

- If they are, are any of the airline or hotel options significantly better or worse?

Are miles and points transfers good value compared to the alternatives?

Yes. Unlike many credit cards, airline miles are excellent value compared to taking shopping vouchers which is the only other option.

1,500 HSBC points gets you 750 airline miles or £5 of vouchers (Amazon, Costa, M&S, John Lewis, Tesco etc) so you are ‘paying’ just 0.66p per airline mile.

Are any of the airline or hotel options significantly better or worse?

Since we always value airline miles at around 1p, at least as long as they are used for premium cabin flight redemptions, we can say that they are a good use of your HSBC points. Compared to taking shopping vouchers, you are ‘paying’ 0.66p per mile which is a great deal.

However, the hotel transfer ratios stink.

The exchange rate from HSBC to hotel points is 2:1 – the same rate as used for airline miles. This is shocking value because, using a very broad generalisation, airline miles are worth double what hotel points are worth.

For example, I value an IHG One Rewards point at 0.4p. This means that 2 HSBC points gets you 0.4p of IHG One Rewards points – but would also get you 0.66p of shopping vouchers! Avoid – unless you need the points immediately, since the transfer to IHG is instant.

Conclusion

HSBC Premier has now established itself as the clear leader in the Visa / Mastercard space for anyone who wants a ‘convertible currency’ that could be moved to multiple travel rewards schemes.

For 10 of the 11 partners (Avios being the exception) it is the only way of earning these points from Visa or Mastercard spend.

(If you DO want Avios, which as this is HfP is likely, then forget HSBC Premier. You are far better off with the free Barclaycard Avios Mastercard or the paid-for Barclaycard Avios Plus Mastercard which has a 25,000 Avios bonus.)

The snag is that you need a HSBC Premier current account to apply for these cards, which requires a £75,000 income and the holding of a HSBC mortgage, insurance or investment product – albeit Premier has decent benefits, including full travel insurance, and is free.

Our full review of the free HSBC Premier credit card is here.

Our full review of the HSBC Premier World Elite credit card is here.

JPK

JPK  Bernard

Bernard  The Original David

The Original David  Nico

Nico  hugo r

hugo r  JD Beds

JD Beds  zapato1060

zapato1060  Josh B

Josh B  exp70

exp70  aseftel

aseftel  JDB

JDB  numpty

numpty  memesweeper

memesweeper  TS77

TS77  Polly

Polly

Comments (27)